Know Why Your Home Loan Application May Get Rejected?

10 Jun 2022

Table of Content

Home loans are usually of a high value and have a tenure of around 20 to 30 years. Thus, lenders follow a well-defined and stringent process to approve and sanction such loans. This ensures that the lenders do not build any NPAs (Non-Performing Assets). Consequently, procuring a home loan is a rigorous process, and if your application gets rejected, you have to start this process all over again. Hence, it can be pretty disheartening to have your home loan application rejected.

Wondering what are some common home loan rejection reasons?

Let’s find out:

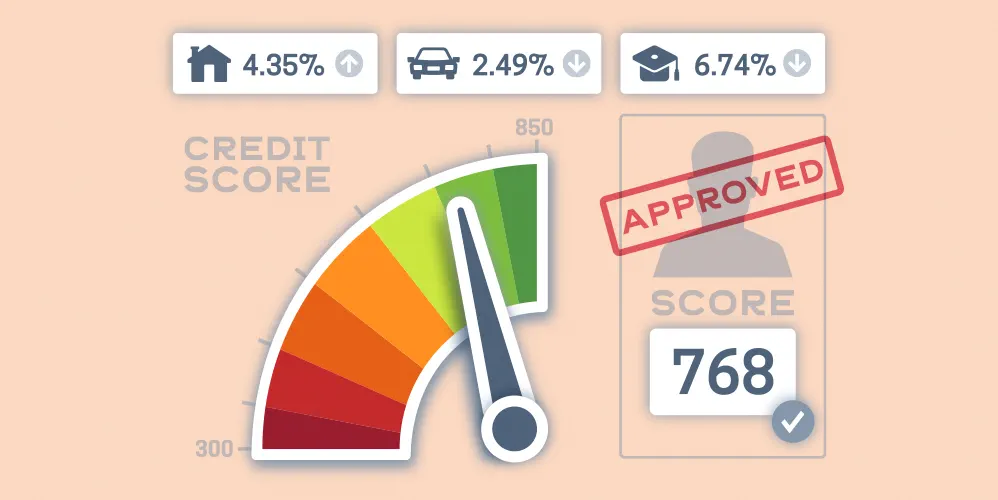

• Low credit score

Your CIBIL score is the summary of your credit history. It ranges between 300 to 900 points. Generally, loan providers consider people having a CIBIL score above 701 to be creditworthy. If you have a CIBIL score below 650, your home loan application is likely to be rejected. If you have a low CIBIL score, ensure you repay your debts on time to build up the score. You should also check your credit reports periodically to ensure that there are no mistakes in them. Thus, you must always be aware of your CIBIL score and maintain it at least above 700 to increase the chances of your home loan request getting sanctioned. A good CIBIL score can also help you procure a home loan at a relatively lower interest rate.

• Frequent and irregular job changes

Home loan providers love stable debtors as they come along with very low risk. These are people who have a steady job or business and are quite secure in their life. On the contrary, changing jobs frequently at short intervals depicts instability. Hence, job hoppers are less likely to receive a home loan sanction. Furthermore, it is also important for your employer to be financially stable as well.

• Incorrect or incomplete documentation

This is one of the most common loan rejection reasons. Your documents play a particularly vital role in the home loan application process. They not only help the lender gain trust in your repayment capability but also ensure that the property is being bought complying the law of land. To increase the chances of your home loan being sanctioned, make sure to compile all the required documents before submitting your home loan application. Additionally, it is also important to keep the loan documents in the same order as required by the lender.

• Existing debts

Home loan providers meticulously gauge your ability to afford EMIs before sanctioning the loan. All your existing obligations are accounted for by the lenders. Your actual income is calculated by subtracting any ongoing repayments from your total income. Thus, having other debts reduces your home loan repayment capability and increases the chances of your application being rejected or sanction of lower loan limit than required. To increase the chances of your loan being sanctioned, it is better to clear off your existing debts before you apply for a home loan. This will not only boost loan repayment capability but also help you manage your finances better as home loans are one of the cheapest forms of debt in the market.

• Not filing your Income Tax Returns

Home loan providers require you to file two years of income tax returns. Even if you are a salaried individual and do not get Form-16 from your employer, you are still required to file your income tax returns. Having a track record of filing your taxes with diligence reflects positively on your home loan application. Income Tax Filing not only shows the creditor that you are a disciplined individual but also help them to understand your repayment capability in a better way.

• Property related issues

Before lending, banks / FIs through investigate the title of the property being purchased. One should check all the property related title documents and other related issues thoroughly. Home Loan applications may be rejected for reasons non-availability of title documents, title of the property is not clear & absolute, litigation/s of serious nature is /are pending etc. To avoid the rejection of your loan due to such reasons, make sure to thoroughly check the ownership details of the property you wish to purchase.

As we can see, a lot of the reasons for the rejection of a loan application can be easily avoided. If you are buying a home for the first time, you can take a lawyer’s help in reading the fine print on the house papers. Many lenders also provide professional help and assistance to home loan applicants to smoothen out the entire process before they issue a loan.

You can also speak with your preferred lender and ask them what things you need to keep in mind to ensure that your loan application goes through smoothly as per their process. As part of this discussion, do also ask them for a complete list of documents needed as well as any doubts you may have on the loan terms and conditions. With complete knowledge, you can make an informed decision while buying your very own home.

All the best.

Popular Articles

Tag Clouds

Related Articles

Guide to Getting Agriculture Loan: Application, Eligibility & Required Documents

-

Disclaimer

The contents of this article/infographic/picture/video are meant solely for information purposes and do not necessarily reflect the views of Bank of Baroda. The contents are generic in nature and for informational purposes only. It is not a substitute for specific advice in your own circumstances. Bank of Baroda and/ or its Affiliates and its subsidiaries make no representation as to the accuracy; completeness or reliability of any information contained herein or otherwise provided and hereby disclaim any liability with regard to the same. The information is subject to updation, completion, revision, verification and amendment and the same may change materially. The information is not intended for distribution or use by any person in any jurisdiction where such distribution or use would be contrary to law or regulation or would subject Bank of Baroda or its affiliates to any licensing or registration requirements. Bank of Baroda shall not be responsible for any direct/indirect loss or liability incurred by the reader for taking any financial decisions based on the contents and information mentioned. Please consult your financial advisor before making any financial decision.

JanSamarth Portal by PM - A Complete Guide

Over the years, the Government of India has rolled out numerous welfare schemes. For instance, there is the Central Sector Interest Subsidy Scheme by the Ministry of Education or the MUDRA Loan scheme under the Department of Financial Service. Users can access these schemes on the respective Ministry's websites. However, tracking applications on various websites can be cumbersome. Keeping this in mind, the government has unveiled the JanSamarth portal, enabling applicants to avail of up to 13 credit-linked government schemes under one roof. Read on to know more about the schemes, its objectives, the registration process and more.

Personal Loan Vs Car Loan - Which Is Better?

Owing a car is a dream for many. A vehicle offers you the convivence of travelling when you want to and saves you from the rush of local commute. Having your own car also helps in times of emergency. With the outbreak of novel coronavirus, using local commute or public transportation can be daunting. Your own vehicle ensures your safety in such trying times.